Buyers who have been waiting for that perfect deal on a home are now finding themselves in a more costly predicament. Record low interest rates over the past few months have made it the best time to buy a home in the fifty years...unfortunately, it doesn't look like they are going to hang around much longer.

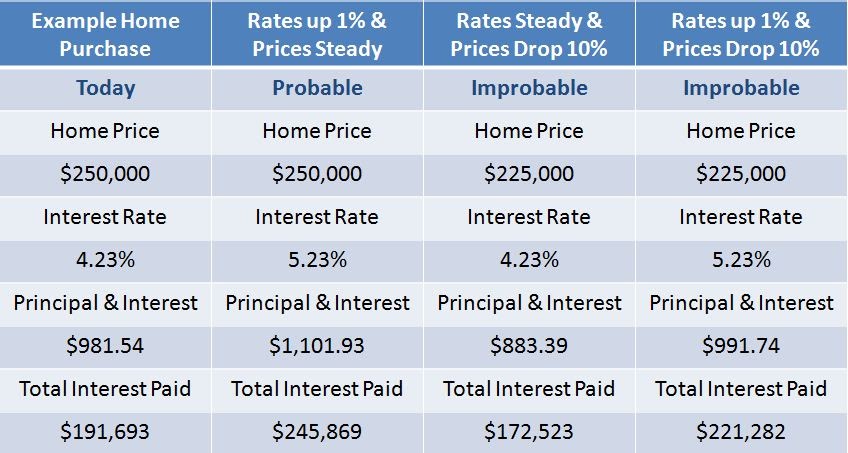

Those who “choose to wait until prices come down more” are gambling that interest rates will hold steady or drop. However, the truth is even a 10 percent drop in home prices is nullified by a 1 percent increase in interest rates. The figure below illustrates how this works for a $250,000 home purchase and the relative likelihood of each scenario.

When thinking about which is more likely: an increase in mortgage rates or a further drop in home prices...consider the findings below based on the last ten years of monthly home price and mortgage interest rate data:

1. A one percent increase in mortgage rates is ten times more likely to happen than a ten percent drop in home prices.

2. A one percent rate increase more than offsets a ten percent reduction in home prices.

3. When interest rates fall by one percent, the total interest paid is almost three times more than the interest savings from a ten percent drop in home prices.

4. The probability of both happening at the same time is ridiculously small, and homeowners would still pay 15 percent more in interest over the life of the loan.

Interest rates have dominated the news in recent months as we’ve shattered record low after record low. Potential home buyers need to understand the positive financial impact low interest rates have on the cost of home ownership and the thousands of dollars that can be saved over the life of a typical mortgage loan.

When you're ready to list your home or if you're looking to buy, feel free to give us a call. We've helped hundreds of families and we'd love to help you!

Email, text, or give us a call anytime...913.787.1870 or

PickettPropertyGroup.com.

Everyone is wanting to know what is going to happen in real estate in the new year. Unfortunately, there is no way to predict one way or another, but there are signs out there indicating that the market is improving. Take a look at these recent statistics:

Everyone is wanting to know what is going to happen in real estate in the new year. Unfortunately, there is no way to predict one way or another, but there are signs out there indicating that the market is improving. Take a look at these recent statistics: